Investor Views on Multi-segment Companies

GE’s November announcement that it will form three public companies has revived a decades-long debate about the future of the conglomerate/multi-segment companies. While our proprietary research finds that 64% of investors prefer pure-plays over multi- industry businesses in general, we’ve identified notable exceptions through our ongoing Voice of Investor® Perception Study research on behalf of our clients. While GE’s notable and necessary move marks an end to an era and the start of new beginnings, it doesn’t signal the end of an era for all conglomerates though we all must have heightened awareness as it does shine a spotlight.

With bellwethers GE, DowDuPont and United Technologies moving to separate their businesses in the past several years, and Toshiba’s recent strategic review announcement, we wanted to share our proprietary research, which reveals significant investor buy-in to the multi-segment/conglomerate approach in certain scenarios.

Following the 2008 Financial Crisis, activist investors have aggressively pushed for the separation of conglomerates or the divestment/spin-off/sale of assets on the thesis that individual businesses as part of a multi-segment conglomerate underperform pure-play peers. So far through Q3 YTD in 2021, there has been a 5.1% increase in activist investors in the U.S. publicly pushing for divestitures, as well as a 54.5% increase in those opposing mergers, relative to the same period last year. (Source: Activist Insight)

The only other types of activist agendas to see increases relative to last year are environmental, governance, and remuneration. All other types – management, M&A, capital structure, operational, shareholder returns and social – have seen decreases year-over-year.

This is particularly true for industrials – the most common sector seeing companies taking a multi-segment approach – which has represented 15% of all activist campaigns globally through Q3 2021 (followed by consumer cyclical, financials, and technology at 13%).

Our primary Voice of Investor® research identifies company profiles most commonly receiving the greatest buy-in to the multi-segment or conglomerate approach are:

- Cash cows (typically from legacy market-leading businesses) fueling investments and acquisitions in a newer, higher-growth business(es)

- Core expertise applied to a diversified mix of businesses

- Earnings compounders

- Countercyclical effects

- Vertical integration

To better understand why investors more commonly support these types of companies, we mined our data:

Cash cows fueling investments and acquisitions in a newer, higher-growth business(es)

“The strategy is to take the cash flow from Segment B and redeploy it in other areas, so if there is a detractor from valuation, it is the fact that none of those are pure-plays, so it tends to create an eclectic investor base. However, Segment A benefits from the cash flow at this time.”

“The strategy is to manage Segment A for market share stability; it is a very strong cash generator. Then, use that to reinvest in Segment B to foster the growth. The portfolio they have today can support the growth outlook they have for the business.”

“Segment B detracts from long-term valuation but it does not mean they should sell it. It is obviously a business in decline. It has been a good cash flow generator and it does not make sense to sell it.”

“At the end of the day, they are doing the right thing as far as harvesting cash. There may be a point in the future if they were able to sell the business and get a good multiple for it, that might be a good strategy, but not at this time.”

Core expertise applied to a diversified mix of businesses

“A lot of the businesses are good, where they have market-leading positions and a competitive advantage that allows them to earn nice returns in those businesses.”

“Their basic strategy sits around a core competitive advantage. All the businesses in their portfolio they want to enjoy some version of that. Using the operating system to drive efficiencies, working with the business leaders to ensure that culture is strong and consistent and that incentives are aligned around their key performance metrics.”

“The strategy now is to deploy capital to make acquisitions in areas that touch faster- growing markets with proprietary technology and high-margin, high-quality businesses. I feel that now that they have articulated the strategy and investors have an objective, they feel like they have the green light to execute that strategy across what is a diversified portfolio.”

Earnings compounders

“The portfolio is in a great place despite being across many businesses and end markets. The company is focused on becoming a high-quality growth industrial business that will continue to compound earnings by redeploying cash flow into new businesses.”

“I agree with their long-term strategy and portfolio approach in terms of compounding growth, acquisitions, applying the business system. It makes a lot of sense.”

“For an industrial compounder, a lot of what they do lives and dies on the quality of the businesses they buy and how they incorporate them. It can work well.”

“The strategy is being a quality compounder, driving recurring revenue growth, improving the operating margin, and deploying the free cash flow that these businesses throw off. Some are better as pure-plays but this model can work.”

Countercyclical effects

“I like Segment B because it is a consistent business, so for me it does not detract but in general, other investors will discount their valuation because they have it. Said differently, if Segment A was a standalone entity, that valuation would be higher than the current business but I like the consistency Segment B brings to offset cyclicality in Segment A.”

“The Company has a number of moving parts and segments, so the diversity of the business and the fact some of them are somewhat countercyclical adds an element of stability to the business, which could be viewed as a strength to some degree.”

“From a portfolio perspective, one of the things we do like is the countercyclical cash flow. When things are going well, they are not going to be as cash generative but at the same time, they do have that downside support of a meaningful increase in FCF in more stressed times. This is a bit different than some of the other exposures that we have.”

Vertical integration

“While it does not seem like it is a focus of the business, it is vertically integrated with their other businesses, so it adds value. I am not sure that is a growth area for the business, but it is part of the vertical integration strategy.”

“Their strategy is to be vertically integrated and have their own center and analytics. It is a strength that they do this all in-house and build the products themselves.”

“I have talked in detail to the company about the perception they are exposed to raw materials. I am not sure I fully buy into that. Given they are vertically integrated and have a supply of adhesives in-house, they are able to offset some of that.”

Usage of Sum-of-the-Parts as a Secondary Valuation Methodology

Sum-of-the-parts, a common technique utilized by activists to evaluate the different businesses in a multi-segment company, has not been as widely utilized by traditional institutional investors. Across more than 16,000 interviews conducted over the last 14 years, fewer than 2% of investors report utilizing SOP as a primary valuation methodology. For multi-segment companies/conglomerates, this percentage remains below 10%, on average.

Across our database, the only types of companies that see more than 30% of investors (<2% of companies!) utilizing sum-of-the-parts are:

- Significantly disparate businesses with no apparent synergies

- Core businesses with a third option-like business (e.g., a financial company with two core businesses and a third strategic investments business)

- Cash cow business facing secular decline (what we call a “melting ice cube”), with a higher- growth business mature enough to now stand on its own

Indeed, mining our data unveils SOP is a part of the conversation but often utilized as a secondary approach with less weight given than traditional metrics and methodologies (i.e., P/E, DCF), particularly due to:

- Challenges in identifying peer comparables for a segment

- Little confidence by the investors’ own admission in terms of estimating the sale price

- Potential for businesses to devalue over time

“We have tried to look at sum-of-the-parts. It is always tough with a lot of these compounders because it is very rare you find the stock actually trading with significant upside to a sum-of-the-parts construct.”

“I do not use sum-of-the-parts. I have the buildup in my model, but I have been completely wrong in terms of what a business could sell for, so that is why I do not rely on these things. It is not very often I do sum-of-the-parts now because the market does not follow that approach too often in reality.”

“You could look at sum-of-the-parts and be dead wrong. The trouble is the parts are at risk of devaluing over time because they are not that great and they do not make sense together. We look at the whole first and then if there is a compelling argument for sum-of- the-parts, we will do it, but we do not use it greatly.”

“I do a sum-of-the-parts analysis from time to time, but it is not a particularly useful technique because there does not appear to be a desire to capture the discount.”

“Sum-of-the-parts is something I am mindful of, but it is not my main valuation framework.”

“The market does not tend to think of it that way. It is almost a theoretical sort of a thing. Sum-of-the-parts generally does not work well.”

“Sum-of-the-parts is a little harder because there are no great comps on their major segments.”

Just as we noted with our thought leadership piece on buybacks in the spring, we have identified a perception wall – as we call these types of sentiment situations – around multi- segment companies/conglomerates that must be changed from a “one-size-fits-all” to an “it depends on the company” mindset. To do so, companies must increase investor confidence in the strategic rationale of the portfolio through deliberate, masterful communication, perform well across different business environments (i.e., cycle – a word I never use!) and keep a consistent pulse on investor sentiment as they are more at risk of activism.

Our Voice of Investor® Perception Study research codifies sentiment toward multi- segment corporations and our industry-leading team of advisors has deep expertise partnering with companies to create shareholder value through insights-driven communication and investment positioning strategies.

- Across all sectors and market caps, our research:

- Measures investor views on business segment trends and KPIs

- Proactively monitors investor sentiment through our proprietary Vulnerability Index, including calls for divestments, sales, and splits

- Positions the board and executives to make more confident decisions around portfolio management

- Has been critical in activist defense strategies

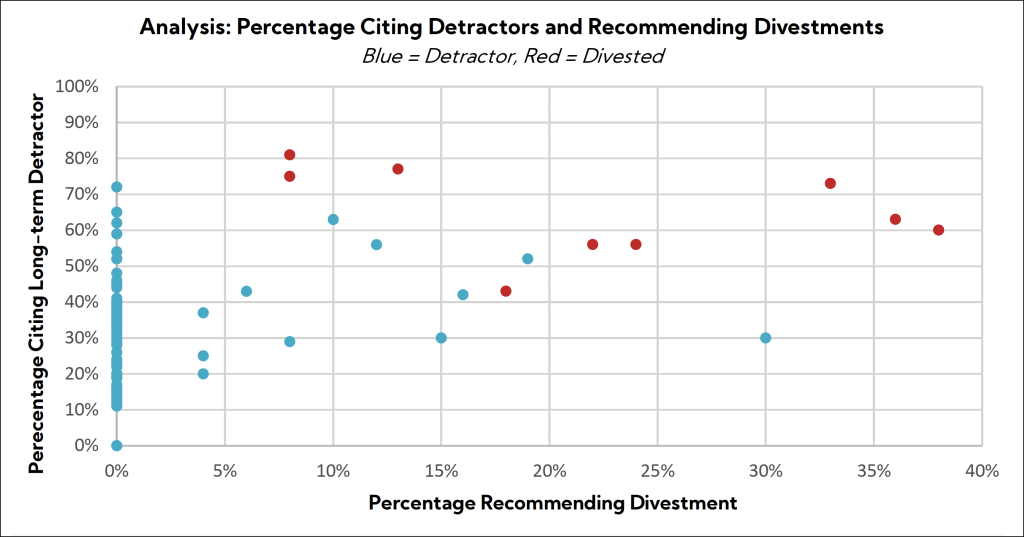

As an example, on how we proactively monitor investor sentiment through our proprietary Vulnerability Index, we measure the percentage of investors identifying a business or asset as detracting from long-term valuation, as well as the percentage of investors calling for divestment. This is a hallmark of our open-ended interview format.

The result: Companies conducting a Perception Study that subsequently spun off assets are outlined in red below, indicating a threshold at which boards and executives took proactive strategic action.

In Closing

We are passionate about the expertise we’ve built to serve as a strategic advisor and give our clients a competitive edge. Portfolio management is serious business and a beacon for activism. Consistently tracking shareholder sentiment on your company, business(es), and portfolio – and the factors that impact your stock’s worth in general – and more importantly, activating around sensible feedback, is one of the most powerful tools to create shareholder value and thwart activism. In the unfortunate event you are approached, a comprehensive repository of investor and analyst sentiment, and specific views and trends on key agenda topics, can (and has) proven itself to be invaluable.