This Week in Earnings – Q3'23

The Sector Beat: U.S. Banks

In today’s thought leadership, we cover:

- Key Events this week

- Key Insights from our 56th issue of Inside The Buy-Side® Earnings Primer®, published last Thursday, October 12th

-

Spotlight on U.S. Banks in The Sector Beat, which provides valuable insight into the U.S. economy, consumer, and deal environment.

Key Events

Employment

- Initial jobless claims, a proxy for layoffs, decreased by 13,000 to a seasonally adjusted 198,000 last week, the lowest level since January. Continuing claims, also referred to as insured unemployment, ticked up 29,000 to 1.73M. (Source: Labor Department)

Fed Meeting

- During his update on Thursday, Federal Reserve Chair Jerome Powell suggested that the recent increase in 10-year Treasury yield will further tighten financial conditions and may act as a substitute for further Fed rate hikes, implying the Fed is on hold now barring clear evidence that stronger economic activity jeopardizes progress on inflation. “Given the uncertainties and risks, and how far we have come, the committee is proceeding carefully.” (Source: WSJ)

Housing

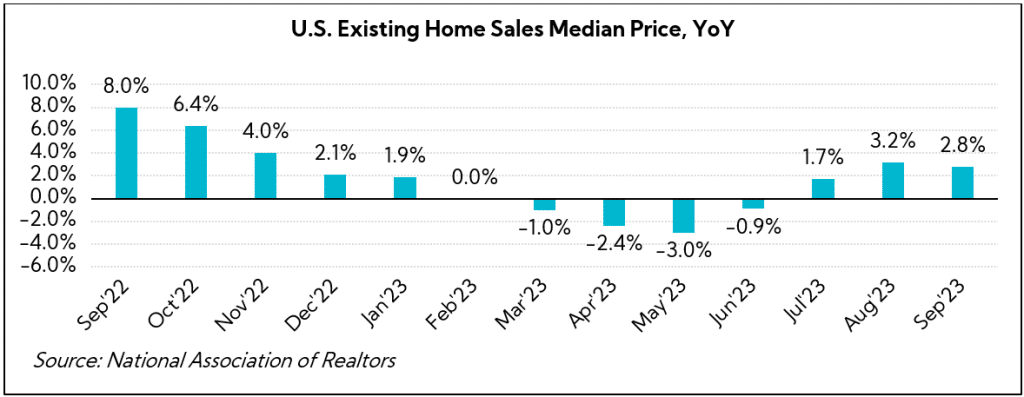

- Home sales fell in September to the lowest rate in 13 years, with sales of previously owned homes on track to be the lowest since at least 2011. Existing home sales, which make up most of the housing market, decreased 2% in September from the prior month and declined 15.4% YoY to a seasonally adjusted annual rate of 3.96M, the lowest rate since October 2010. (Source: U.S. Census Bureau, National Association of Realtors)

- The median price for existing homes was $394,300 in September, up 2.8% YoY and representing the third consecutive month with pricing increasing relative to the prior year. (Source: National Association of Realtors)

War in Israel

- On Wednesday, the Biden administration announced that the U.S. is providing $100M in humanitarian assistance for the Palestinian people in Gaza and the West Bank to “help support over a million displaced and conflict-affected people with clean water, food, hygiene support, medical care, and other essential needs.” The aid is to be administered through the assistance of UN agencies and international NGOs. (Source: The White House)

China

- In Beijing on Wednesday, Russian President Vladimir Putin met with Chinese President Xi Jinping along with more than 130 other countries at the Belt and Road Initiative (BRI) Summit, celebrating 10 years since Xi launched the infrastructure project aimed at strengthening alliances with Asian, African, and Latin American nations. Regarding the Israeli-Hamas war, China and Russia have both called for ceasefire and have declined to explicitly condemn Hamas. (Source: Reuters)

Key Insights

Inside The Buy-Side® Q3’23 Industrial Sentiment Survey®

From our 34th issue of Inside The Buy-Side® Industrial Sentiment Survey®, published yesterday, October 19 — a good indication of how investors and analysts feel about one of the largest sectors of our economy

Following last quarter’s survey that identified increasingly more cautious investor sentiment and more pronounced management optimism heading into Q2 earnings season, the Voice of Investor® captured in this quarter’s Industrial Sentiment Survey® finds Neutral to Bearishviews meaningfully shifting to Neutral while perceived executive tone continues to largely be described as Neutral to Bullish to Bullish, but with some notable easing.

Based on responses from 56 sector-dedicated participants globally, from September 5 to October 11, 2023, comprising 70% buy side and 30% sell side, and equity assets under management totaling ~$6.4T:

Greater Neutral and Slightly More Optimistic Sentiment Captured this Quarter, While Upbeat Management Tone Ebbs Somewhat; Focus on Inflation and Interest Rates Is On the Rise

- Investors characterizing their sentiment as Neutral increases to 48%, up from just 17% last quarter, with most notably rotating out of the Neutral to Bearish camp, which dropped to just 14% from 42% QoQ

- 50% describe executive tone as Neutral to Bullish or Bullish, down from 59% last quarter

- Outright bearishness across sentiment and perceived executive tone remains under 10%, as it has throughout 2023

- 64% expect Industrial earnings to Meet consensus, with more optimism around EPS and FCF performances QoQ; views on operating margins are decidedly mixed

- 50% or more expect companies to Maintain 2023 outlooks

- Inflation and related Pricing Power lead earnings calls topics of interest; Supply Chain (31%), Inventory and Destocking (28%), and Labor (25%) all move up materially QoQ

Broad-based Industrial Weakness Built In with Increasing Concern about “High Valuations” amid a “Higher for Longer” Interest Rate Environment; Debt Paydown Is the Leading Preferred Use of Cash with Fewer Supporting Growth Capex

96% expect broad-based Industrial Weakness:

- 58% either already see or expect weakness in 2023 while 38% suggest it will materialize in 2024

- In light of slowing growth, 68% report prioritizing margins over growth at this time

- Still, expectations for 2023 Industrial organic growth improve to 5.3% on average, up 150 bps QoQ; in Q2, S&P 500 Industrials delivered 4.0% sales growth, on average

Demand (53%) is the leading identified concern for the second consecutive quarter; meanwhile, Interest Rates (51%) and Geopolitical Risks (49%) grew QoQ to become the #2 and #3 global concerns:

- Geopolitical Risk sees the largest QoQ increase with 93% explicitly citing China as the main driver

- Debt Paydown (64%) reclaims the top spot as a preferred use of cash, overtaking Reinvestment (46%)

- Just 3% of investors support Increasing growth capex at this time, receding from >20% in the past two quarters, and off the high of 45% in Q4’22

North America Remains a Bright Spot and China Out-of-favor; Defense Leads in Bulls while Bears Pile into Ag, Auto, and Non-Resi

- North America remains the most compelling region (71%), a consistent QoQ trend, while APAC (ex-China) gains ground as an economy expected to Improve – 59% up from 39% last quarter

- Risk aversion to China continues to grow as 73% now assign a High or Very Highlevel of risk to companies with exposure, up from 65% last quarter

- Growing geopolitical concerns lead to increased Bullishness in Defenseand Commercial Aero

- Ag and Auto see biggest increases in negative sentiment, becoming the #2 and #3 most bearish sub-segments, respectively, after Resi Construction

The Sector Beat: U.S. Banks

At a fundamental level, U.S. Banks appear to have made it through Q3 fairly well. Net interest income generally came in better-than-expected as companies were able attract and price deposits at more favorable levels versus their smaller peers, while improved capital markets businesses aided some of the earnings beats.

However, in line with the sentiment found in our Inside the Buy-Side® Earnings Primer® and Industrial Sentiment Survey®, there was a lot of verbal hedging of these results by management teams on their calls, with many pointing to the current rising macro and geopolitical risks and those on the horizon.

M&A remains largely out of favor, partially a function of the current macro uncertainty and a higher interest rate environment. However, it is also indicative of the fact that investors have made it abundantly clear to companies that they are not in favor of transformational deals — something we have consistently observed in our proprietary research over the past year. Bank executive commentary point to 2024 as a better year for M&A, but visibility on when these conditions will change is opaque. As Bank of America CFO Alastair Borthwick put it, “Investment banking can come back very, very quickly. It’s just that we’ve grown tired of predicting when that might be.”

Another issue is the consumer, which continues to remain a key focal point throughout executive commentary and Q&A, with many of the U.S. Banks suggesting the consumer and small business remain “healthy,” but adding a side of skepticism about how long this state can last. Big Banks’ clientele tend to have strong credit scores on average (e.g., Bank of America’s average credit score was 774 in the latest quarter, above the national FICO average of 7161). Still, credit conditions are seen as increasingly tightening as consumers “manage their budgets” and “normalize” spending patterns from the pandemic-induced spending binge. The leading edge of potential problems with consumer banking this cycle could start in credit cards, where debt levels have been skyrocketing in the face of depleting consumer savings. As a result, we are seeing card companies like Discover increase their reserves in preparation for what could be a bumpier ride for consumer banking during the coming year and perhaps beyond, especially as student loan payments resume this month and cut into other discretionary expenditure buckets.

Furthermore, lower-income borrowers are likely already seeing larger credit problems than the averages portray, which is corroborated by the fact that credit card delinquency rates among smaller banks (i.e., those outside of the top-100 by size) are hitting new all-time highs, to the tune of 7.5%.2 The direction of employment and wages in 2024 will perhaps be more critical factors than ever before for determining the sensitivity around consumer sentiment and impact, and, ultimately U.S. GDP growth.

Key Earnings Call Themes

Executives Continue to Express Caution as the Latest Injection of Geopolitical Uncertainty Further Weighs on Macro Outlooks; “There Are Reasons to Remain Vigilant”

- Goldman Sachs ($119.9B): “Though the U.S. economy has proven to be more resilient than expected, there are reasons to remain vigilant. Treasury rates have risen sharply. On top of that, recent inflation and employment data has come in above estimates, driving market expectations of higher-for-longer interest rates. And there are still a number of sectors in the economy that have yet to absorb the impact of higher rates. At the same time, there has been an escalation of geopolitical stresses around the globe, including the war in Ukraine, ongoing tensions with China, and now the conflict in the Middle East. Overall levels of risk are more elevated than we’ve seen in quite some time.”

- Fifth Third Bancorp ($17.0B): “The base case we’re using continues to assume that the market is a little bit too bullish on the idea of a soft landing here…when you then look at declining real incomes, the only thing standing between somebody who is having to work two jobs and still suffering from a declining real income and credit delinquency is the fact that there was the stimulus buffer that built up because people had forbearance on loan portfolios and stimulus dollars. Well, the student loans are back now. Housing inflation is still very high at 7.2%. And those are just early indicators that that there are people across the country that are struggling a lot more than the headline numbers would suggest.”

- JPMorgan Chase ($420.4B): “There has been an extraordinary amount of fiscal monetary stimulus still in the system and it can drive market sentiment in sales and profits and all that, but you can’t stay like this forever. Between QT and how much of the fiscal stimulus could continue at this rate, you will have the crowding out factor. People have to be very cautious and the geopolitics is just an extraordinary issue we have to deal with. How do you prepare the company for that? We do 100 stress tests a week, and we do multiple views of it, including geopolitical problems and interest rate problems; usually, geopolitics presents itself as a deep recession or a mild recession, or a recession in part of the world, or results in markets going down a lot. And because markets do well is not a reason, ever, to say they’re going to continue to do well.”

- Atlantic Union Bankshares ($2.2B): “We don’t foresee that uncertainty ending anytime soon with recent geopolitical events and a possibly contentious process for the next round of congressional funding. But for the time being, we remain cautiously optimistic in our outlook.”

- Discover ($21.2B): “This quarter, we increased our reserves by $601M, and our reserve rate increased by 22 basis points to just over 7%. The reserve increase reflects a modest deteriorating macroeconomic outlook, increasing delinquencies, and higher loan balances. Our macro assumptions reflect a relatively strong labor market, but also consumer headwinds from declining savings rates and increasing debt burdens.”

Activity Predictions Vary from Bank to Bank, Though Most Concur Deal Activity is Primed to Accelerate Off a Low Base Once Macro Sentiment Improves

- Morgan Stanley ($121.3B): “The minute you see the Fed indicate they’ve stopped raising rates, the M&A and underwriting calendar will explode because there is enormous pent-up activity…I don’t know if it’s six months out or nine months out or it starts three months out from this, but this thing is going to start turning. And then rates will be the kicker. When they start coming down, people will be less focused on cash and accounts, more focused on investment opportunities. That’s when you’re going to see the double kicker.

- JPMorgan Chase ($420.4B): “Current levels in investment banking remain quite depressed even relative to 2019. We do eventually think we’ll recover to those levels and hopefully recover to above those levels, recognizing by the time it happens you will have had many years of economic growth in the meantime. And to be fair, while the current environment is a little bit complicated and mixed and there are some headwinds, things have improved a little bit. I would say our banking team is a little bit more optimistic than they were last quarter.”

- Goldman Sachs ($99.3B): “The IPO market has started to reopen. Since Labor Day, there have been four marquee IPOs priced in the U.S.: Arm Holdings, Instacart, Klaviyo, and Birkenstock. Given the execution of these transactions, I’m encouraged by the prospect of a wider reopening of capital markets. If conditions remain conducive, I expect a continued recovery for both capital markets and strategic activity.”

- Citigroup ($77.2B): “A lot of companies with their industries transforming are really wanting to think big. We’ll see that unlocking when sentiment improves further and companies accept the new pricing reality, which will be helped by a rebound in equity markets. That obviously, from our end, takes quite a few quarters to materialize into revenue just given the nature of the product. So, it’s there, but given where everything is geopolitically and particularly from the macro, no one is going to make that call as to when we’re going to see that sustainable turn in banking at this point.”

- First Horizon ($77.2B): “The [consolidating] M&A environment is likely to be very, very minimal over the next couple of years. Part of that is economic. Part of that is interest rate marks. And, as demonstrated over the last few quarters, uncertainty about regulatory approval processes in addition to the proposed rules around Basel III make anything unlikely in the near term. Our view is it’s anywhere from 1.5 years to 3 years before you really start to see a pickup in M&A activity.”

A Recurring Theme, Execs Caution Over Pending Basel III Endgame Proposals* that Could Ratchet Up Capital Requirements Including Coverage of Accumulated Other Comprehensive Income (e.g., Unrealized Losses)

Unrealized Losses

- Ally Financial ($7.4B): “With Basel III Endgame, the biggest impact for us is in terms of our accumulated other comprehensive income (AOCI). We can manage within that transition time period that it’s been proposed so far without doing anything unnatural. That is we can manage it organically [but] as you can imagine, it’s obviously curtailed our share repurchases…and it’s also forced us to really make hard decisions around the growth trajectory of some of our growth businesses.“

- Fifth Third Bancorp ($17.0B): “Our balance sheet is elevated due to a couple of reasons. One, the unrealized losses, whether you have it in available-for-sale or held to maturity, you do have to fund those losses in your liquidity buffers. And so, should those losses come down, that certainly frees up cash to shrink the sheet…Both of those things are going to be measured more in years than in quarters in terms of the cash coming down.”

- Bank of New York Mellon (32.9B): “We have about $2.3B of unrealized losses in our available-for-sale portfolio and we expect about half of that to come back into capital over the next 12 months. So, from where we sit here today, we continue to build capital. We feel very good about our capital position. Ratios are healthy. Liquidity is healthy.”

Basel III Endgame

- JPMorgan Chase ($420.4B): “The current proposal exacerbates existing features that discourage beneficial scale and diversification. If it goes through as written, there will likely be significant impacts on pricing and availability of credit for businesses and consumers.”

- Goldman Sachs ($99.3B): “There are certain businesses that we might reduce our activity level because, with the new capital rules, the returns don’t look attractive. And obviously, the Europeans, if this was implemented this way, would have an advantage. [Still] our belief is we’d be able to optimize and pass on pricing in a reasonable way. We’d have to look at the final rules; we’d have to adjust. It will affect behavior, it will affect pricing, it will affect optimization, but I know everybody wants to jump to the clear answer. You need to see the rules and then institutions and end users need to adapt to the new reality, whatever it is.”

*Basel III is an international regulatory framework designed to strengthen the stability of the global banking system. Developed in response to the 2007-2008 financial crisis, it mandates banks must maintain higher levels of capital reserves and adhere to new standards for measuring risk, liquidity, and leverage. The Basel III endgame refers to the final set of reforms to the Basel III standards that were released on July 27, 2023 and must be complied with by July 2025 during this multi-year transition period.

Office Category Continues to Perform Sub-optimally, with CRE Generally Considered a “Wild Card” in the Coming Months as Banks Pad Their Reserves

- Synovus Financial ($3.9B): “The one question mark and wild card for 2024 will be what happens with the pay off and pay down activity in CRE. As you know, we haven’t seen a very constructive marketplace there given where cap rates and interest rates have moved and so we haven’t had a lot of payoffs and pay downs.”

- Truist ($37.4B): ”Something that we try to control is our efforts to get ahead of the CRE office risk. In Q3, we were very intentional about working through moving from just identifying the risk to resolving several of the problem credits. And we took some losses there to do that. And we’re anticipating opportunities to do more in Q4.”

- Wintrust Financial ($4.8B): “As noted in our last few earnings calls, we continue to be highly focused on our exposure to commercial real estate loans, which composed roughly one-quarter of our total portfolio. Higher borrowing costs and pressure on occupancy and lease rates are cause for concern, particularly in the office category.”

- Zions ($4.8B): “Credit quality measures for the total CRE portfolio remain relatively strong, though nonperforming assets increased in the quarter to 2.3% of the office portfolio. As mentioned, we recognized $3 million in losses on two office loans in the quarter across the CRE office portfolio.”

- U.S. Bancorp ($51.4B): “When you end up looking at the industry, I think there is some tightening that’s going on out there. If you end up looking at our situation, the area that we’re monitoring the most is commercial real estate, office space specifically. We have a reserve that’s about 10% of the overall balance there. We have been increasing that and we’re likely to continue to increase that because that’s going to be a pressure point.”

While Entering “This Cycle” from a Point of “Strength”, Mass Market Consumer Spend Continues to Retrench While Credit Card Delinquencies Tick Higher

- Goldman Sachs ($99.3B): “I am hearing as I interact with CEOs particularly around consumer businesses, some softness, particularly in the last eight weeks, in consumer behaviors. I don’t want to over-amplify that because the economy and the consumer has been more resilient.”

- Discover Financial Services ($21.2B): “Our revolver base, we’re seeing a more significant decrease in sales activity, which makes sense as they try to manage their household budget. We’re seeing accounts that transacted in 2021, 2020, and 2022 beginning to revolve more. So the revolve rate is back to where we were historically. My expectation is that delinquencies will slow in the first half of 2024. If that doesn’t happen, that’s an indication that the stress that the consumers are seeing is more significant than what we’re observing today.”

- U.S. Bancorp ($51.4B): “The consumer is entering this cycle in very strong shape. From a balance standpoint, from the perspective of savings accounts that they have, the spend activity, all of these are starting to normalize to a pre-pandemic, normal level. The companies and small businesses are also in very good shape.”

- Fifth Third Bancorp ($17.1B): “Clients are seeing a gradual slowdown that is essentially disposable income. They’re seeing disparities on the consumer side between either the businesses or hotels that cater to retired people or to high-end consumers in high-end destinations that continue to do well, whereas the mass market properties are starting to soften.”

Credit Tightening

- Wells Fargo ($150.9B): “We’ve been incrementally tightening the credit box on the consumer side for a while…it’s really across the board in home lending, auto, card, personal loans, really every single one of them had some credit tightening. And it’s been a bit incremental over the last four or five quarters.”

- United Community Banks ($2.8B): “While we do expect credit to tighten and the credit losses economically to struggle in the future because of credit tightening and the rapidly increasing interest rates, we’re not really seeing anything to speak of yet.”

- Truist ($37.5B): “We don’t necessarily see a big shoe [dropping]. The biggest impact we’re trying to evaluate through as you shift from a long secular low-rate environment to where we are now is how economic some of those deals were even if you thought you’re underwriting well, how sustainable will all that be. We feel good about where we are, and I’d say generally, the industry as well.”

If you woke up with perfect macro and geopolitical amnesia and just read the headlines of this Big Bank earnings season, you would say they are doing quite well — solid profits, strong capital positions, and still relatively little in the way of credit problems. However, there is a growing list of risk factors lurking ahead for the banking sector — whether they be rapidly changing interest rates across the curve, increased rate competition for core deposits, peak employment and peak consumer health, rising geopolitical risks, increasing commercial real estate loan problems, the impacts of pending liquidity regulations, or ballooning unrealized losses in held-to-maturity securities portfolios. No matter what happens, it is increasingly clear that guiding the Street for 2024 will be a larger-than-normal challenge for many companies — especially for the Banks.

Conservatism will again be the strategy and as we have consistently shared with our clients since Q3’21, bullish on our company, not on the macro!

We’ll be keeping our eyes and ears on the ground as this earnings season unfolds, and we hope you’ve found our Inside The Buy-Side® publications timely, insightful, and helpful as you prep for your upcoming calls.